Why Physical Still Works for Many People

Digital budgeting tools — apps, spreadsheets, aggregators — are genuinely useful for many people. They automate categorization, provide visual dashboards, and connect directly to accounts. They also get ignored, deleted, forgotten, and abandoned by a substantial portion of people who try them.

The reason physical budgeting works for some people who fail with digital tools is tangibility. Writing numbers by hand engages a different cognitive process than tapping entries into an app. Physically seeing money allocated in envelopes or on paper creates a different relationship with those numbers than seeing them in a database.

If you’ve tried multiple budgeting apps and abandoned each one, a physical system might be your fit — not because it’s objectively superior, but because the physical engagement works better for how your brain processes information. This isn’t a technological regression; it’s honest self-knowledge.

The Basic Budget Binder Components

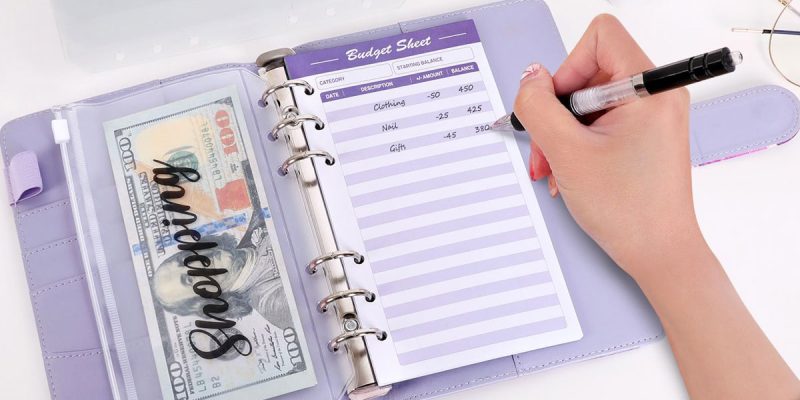

A budget binder is simply a physical system for tracking your finances — usually a three-ring binder with dividers and printed or handwritten tracking sheets. The components that most budget binders include:

Income tracking page: a place to record all income for the month, including irregular or side income alongside regular salary.

Budget page: your monthly budget allocations by category — what you plan to spend in each area before the month begins.

Expense tracking pages: a daily or weekly log of actual spending, categorized to match your budget. Writing these by hand rather than relying on automatic app categorization forces active engagement with every transaction.

Savings goals tracker: a visual progress indicator for each savings goal (debt payoff, emergency fund, vacation fund, etc.). The visual element — watching a bar fill up or a debt number decrease — provides motivation that abstract digital numbers often don’t.

The Cash Envelope Integration

Budget binders and cash envelope systems work particularly well together. The binder holds the tracking and planning; the envelopes hold the actual cash for discretionary categories.

At the start of the month, you withdraw cash for your variable spending categories (groceries, dining, personal care, entertainment) and distribute it to labeled envelopes. Spending from the envelope is automatically tracked — when the envelope is empty, the budget for that category is spent. No apps, no receipt accumulation, no end-of-month reconciliation.

The binder records the starting amounts and any mid-month adjustments (moving money from one envelope to another deliberately). The combination provides both the behavioral constraint of physical cash and the planning and review function of written tracking.

Customizing Your Binder for Your Life

The most useful budget binders are designed around the specific complexities of your financial life rather than generic templates. Some people need detailed irregular expense tracking. Others need a simple overview. Some benefit from goal visualization pages. Others need debt payoff tracking charts.

Free budget binder printables are available online in enormous variety — a search for your specific need will produce dozens of options. Customizing a binder that reflects your actual income, expense categories, and goals takes an afternoon and produces a tool that’s genuinely useful rather than a generic template that doesn’t fit.

For people who are self-employed or have variable income, the binder’s income tracking page is the most important component — logging all income sources for the month alongside a running year-to-date total provides visibility that makes quarterly tax planning and cash flow management significantly more manageable.

Making It a Monthly Ritual

The budget binder works as a habit, not as a one-time setup. The monthly ritual of setting up a new month’s pages — writing in the income expectation, filling in budget allocations, preparing tracking pages — takes 30 minutes and creates intentional financial engagement once per month.

Pair this setup ritual with a specific time (first of the month, first weekend of the month) and a specific environment (same chair, same drink, same quiet) and it becomes an appointment rather than a task. Monthly appointments you keep beat daily apps you gradually ignore.

End-of-month review — comparing plan to actual, identifying where the gaps were, adjusting next month’s budget accordingly — takes another 30 minutes and is where the most learning happens. The person who spends one hour per month actively engaging with their finances in this way usually outperforms the person with the most sophisticated app but no consistent engagement.