Where the Rule Comes From

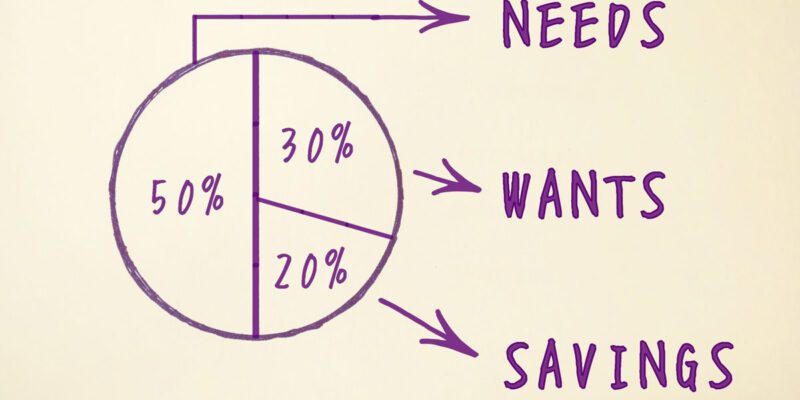

The 50/30/20 rule was popularized by Senator Elizabeth Warren and her daughter Amelia Warren Tyagi in their 2005 book “All Your Worth.” The idea is straightforward: take your after-tax income and split it into three buckets. Fifty percent goes to needs (rent, groceries, utilities, minimum debt payments). Thirty percent goes to wants (dining out, entertainment, subscriptions, travel). Twenty percent goes to savings and any extra debt repayment.

It sounds clean. It sounds simple. And honestly, as a starting framework for someone who’s never budgeted before, it’s genuinely useful. The problem is when people treat it as a universal law that works identically for a 24-year-old in Austin and a 45-year-old in Manhattan raising two kids.

The Case For It

Let’s give it a real defense first, because there’s a reason this rule spread so far. It’s easy to explain, easy to remember, and it stops the endless paralysis of “how exactly should I categorize my spending?” Most budgeting systems fail because people spend more time categorizing and second-guessing than actually changing behavior.

The 50/30/20 rule gets you moving. If you’re someone who has never seriously thought about where your money goes, adopting these three buckets and trying to roughly hit the percentages will almost certainly improve your financial situation. The 20% savings target especially is a meaningful benchmark. Many financial advisors actually consider 15-20% a solid savings rate for most people at most income levels and life stages.

There’s also something psychologically healthy about the 30% “wants” category. Unlike extremely restrictive budgets that feel punishing, giving yourself explicit permission to spend 30% on things you enjoy makes you far less likely to go on a guilt-fueled binge spending spree. Rigid budgets create resentment. Resentment leads to abandonment.

Where It Falls Apart

Here’s where I have to be honest about the rule’s real limitations.

In major cities, the 50% needs target is often impossible. If you live in Nairobi, London, New York, or any expensive metro area, rent alone can eat 40-50% of your take-home pay. That leaves no room for food, transport, utilities, or any other necessities. The rule was designed around median American incomes from 2005. The housing market has changed dramatically since then.

Lower incomes break the math entirely. If you’re earning minimum wage or a modest salary, you might need 70-80% just to cover basic needs. Telling someone in that position to cap needs at 50% isn’t budgeting advice, it’s economic fiction.

The needs vs. wants line is blurrier than it looks. Is a Netflix subscription a want? Probably. Is a gym membership a want if exercise is your primary stress management tool and you have a desk job? Harder to say. Is a slightly more expensive apartment in a safer neighborhood a need or a want? The categories create more debate than they solve for a lot of people.

The savings category also conflates very different goals. Twenty percent “savings” could mean retirement contributions, emergency fund building, paying off high-interest debt, or saving for a down payment. These things have different urgencies and different optimal approaches. Lumping them together can cause people to under-prioritize debt payoff, which is almost always the highest-return financial move available.

Real Life Example: How It Plays Out

Let me give you a concrete example. Imagine someone taking home $3,500 a month after tax. The rule says: $1,750 needs, $1,050 wants, $700 savings. In a mid-size city with reasonable rents, that’s workable. Rent $900, utilities $100, groceries $250, transport $200, phone $60. That’s $1,510 in needs. There’s even a little breathing room in the needs category.

Now take someone in the same situation but renting in a more expensive city where a modest one-bedroom runs $1,600. Their needs are already $2,110 before food, transport, or utilities. The math simply doesn’t work without either earning more, spending less on needs (practically impossible), or accepting that the percentages need adjustment.

The honest version of using this rule is to treat it as a target and a direction rather than a precise prescription. If your needs are at 60%, that’s useful information. Your goal becomes gradually reducing that percentage as income grows, rather than feeling like a failure because you’re not at 50% yet.

How to Adapt It for Your Situation

If the standard percentages don’t fit your income or location, adjust them intentionally. The principle underneath the rule (separate needs from wants, protect savings) is more important than the exact numbers. Some financial planners suggest a 60/20/20 split for people in high cost-of-living areas. Others use 70/10/20, keeping savings sacred even when wants have to shrink.

The key adaptation most people need is to rank their savings goals. If you have high-interest credit card debt, paying that off should be part of or even the entirety of your “savings” percentage for a while. A credit card charging you 22% interest is guaranteed to cost you more than almost any investment return you’d get by keeping that money elsewhere.

Review the percentages quarterly, not just when something feels off. Income changes, life changes, rent changes. A budget built for your life six months ago may need adjustment today.

The Bottom Line

The 50/30/20 rule is a good starting framework and a genuinely terrible fixed rule. Use it to get started, to understand where your money is going, and to have a target to aim toward. Don’t let it make you feel like you’re failing if your situation doesn’t match the ideal percentages.

If I had to recommend it: use it for the first three months of getting serious about your finances. By then, you’ll have enough real data about your actual spending that you can create something more tailored to your life. The goal of a budget isn’t to follow the right rule. It’s to make deliberate decisions about your money instead of just watching it disappear.